The Startup Column:Reassessing the Startup Ecosystem of Taiwan’s Six Major Cities – Taipei

As Taiwan’s political and economic center, Taipei continued to serve as a key engine driving domestic startup development in 2025. According to leading international rankings, the city’s startup ecosystem remains highly competitive on the global stage:

● Global ranking: Taipei ranked 54th worldwide in the Global Startup Ecosystem Index 2025 published by StartupBlink.

● Position in Asia: In the Global Startup Ecosystem Report 2025 by Startup Genome, Taipei ranked 18th in Asia, maintaining a leading position among emerging startup markets in Asia.

Taipei hosts the highest concentration of accelerators, incubation centers, and innovation hubs in Taiwan, and is also the primary base for investment institutions. This has established the city as a preferred destination for both domestic and international entrepreneurs.

1. Startup Development: Size and Growth Trends

1.1 Overall Size and Growth

According to data from the FINDIT Taiwan Startup Information Platform as of the end of October 2025, Taipei is home to a total of 4,253 startups, accounting for approximately 42.4% of all startups in Taiwan and ranking first nationwide. Since 2010, the number of startups has shown a consistent upward trend, with more than 400 new companies established each year. Although the pace of growth has moderated slightly since 2021, the overall number of startups continues to expand steadily.

Fig. 1: Number of Startups Established in Taipei

1.2 Geographic Distribution

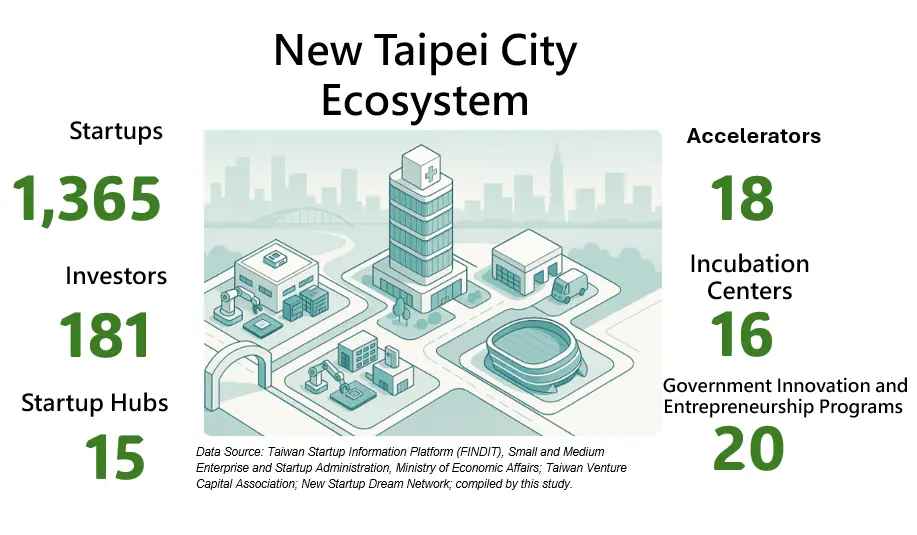

The geographic distribution of Taiwan’s startup ecosystem exhibits a clear north-south divide. Taipei leads by a significant margin in terms of the number of startups, followed by New Taipei City with 1,365 companies. Major metropolitan areas in central and southern Taiwan each host approximately 800 to 900 startups, while Hsinchu, known for its strong focus on technology R&D, accounts for 678 startups.

Fig. 2: Number of Startups in the Six Special Municipalities and Hsinchu Region

2. Key Sectors

Compared with other regions that tend to focus on manufacturing or hardware, Taipei’s industrial profile is characterized by a strong concentration in biotechnology alongside a high degree of diversification. An analysis of the 4,253 startups by sector shows that the top five industries collectively account for approximately 40% of the total.

Fig. 3: Distribution of Key Sectors of Startups in Taipei

3. Capital Market Performance: Funding and Exits

3.1 Investment Overview

Access to capital is a critical driver of startup growth, and Taipei demonstrates strong ability to attract capital. As of the end of June 2025:

- Number of funded startups: A total of 977 startups have secured funding.

- Total funding amount: Disclosed investments reached NT$235.07 billion (approximately US$7.68 billion).

- Average deal size: The average funding amount per deal was approximately NT$127 million, including 33 large-scale transactions exceeding NT$1 billion.

- Most favored sectors by investors: While biotechnology accounts for the largest number of startups, energy ranks highest by share of funded startups, at 67.4%. This is followed by health care (37.1%) and hardware (28.4%), reflecting strong capital market interest in the energy transition.

3.2 Recent Major Investment Deals

The following section highlights the top five largest deals over the past year among Taipei-based startups.

Tab. 1: Funding Activity of Startups in Taipei Over the Past Year

|

Company Name |

Date |

Round |

Amount (NT$) |

|

KKday.com International Co., Ltd. |

Dec 2024 |

Series C+ |

2.28 billion |

|

Botrista Technology Taiwan Co., Ltd. |

Jul 2024 |

Series C |

2.12 billion |

|

EPFM DE LLC Taiwan Branch (U.S.A.) |

Mar 2025 |

Series A |

1.27 billion |

|

Graid Technology Inc. |

Mar 2025 |

Series B |

990 million |

|

Elixiron Immunotherapeutics Inc. |

May 2025 |

Series B |

660 million |

Data Source: Taiwan Startup Information Platform (FINDIT)

3.3 Exits

Exits are a key indicator of ecosystem maturity. To date, 96 Taipei-based startups have achieved successful exits through IPOs or mergers and acquisitions (M&A):

- Exit channels: Listings on the Emerging Stock Board (ESB) account for the majority, with 47 companies (nearly 50%), followed by M&A transactions (15%).

- Recent deals:

- M&A: Acquisitions include SYSTEX Corporation’s acquisition of Neweb Information (July 2024) and Xxentria Technology’s acquisition of Kuobrothers Corp. (February 2024).

- IPO / ESB: Software startup GrandTech Cloud Services listed on TPEx (July 2025); biomedical startup aetherAI listed on the ESB (November 2024); and UnicoCell Biomed transferred from the Taiwan Innovation Board to a TWSE listing (October 2025).

4. Investment Institutions

As Taiwan’s financial center, Taipei hosts 891 investment institutions, accounting for 38.3% of the national total, well above other cities and counties. In terms of investor composition, Taipei differs from the Hsinchu region, where corporate venture capital (CVC) dominates (accounting for 80%). In Taipei, funding sources are more balanced and diversified, with venture capital (VC) and corporate venture capital (CVC) each representing approximately 50%. This balanced capital structure is well suited to supporting startups across different stages of development and industry sectors.

5. Conclusion and Outlook

The data indicate that Taipei, home to more than 4,000 startups and nearly 900 investment institutions, has firmly established a leading position in Taiwan’s startup ecosystem, supported by its strong concentration of resources. Looking ahead, Taipei is actively transitioning from a standalone city-level competitor to a central driver of the broader ecosystem. By strengthening partnerships with other cities that offer complementary strengths, such as Hsinchu’s expertise in hardware R&D and Taoyuan’s manufacturing capabilities, Taipei is positioned not only to remain Taiwan’s innovation core, but also to serve as a key link in the global startup ecosystem value chain.

![[ 2025 Taiwan Startup Investment Trends Annual Report – Overview ] Resilience and Challenges: Insights from Taiwan’s Startup Investment](https://findit.org.tw/Files//ResArticle/dea67192-bcf0-4611-b9fd-456b224b54ef.webp)