[ 2025 Taiwan Startup Investment Trends Annual Report – Overview ] Resilience and Challenges: Insights from Taiwan’s Startup Investment

In recent years, the global venture capital market has continued to cool, resulting in an increasingly cautious investment climate. Yet Taiwan’s startup investment landscape has demonstrated countercyclical growth. In 2024, total investment surpassed NT$100 billion, reaching a ten-year high. Although the number of deals declined slightly, the continued increase in average deal size suggests that capital is becoming more concentrated in high-potential startups.

By sector, hardware, health care, and energy remain the primary investment areas, while sustainability and circular-economy sector has rapidly emerged as a new focus. On the investor side, corporate investment (CVC) continues to dominate, and the National Development Fund (NDF) has leveraged various investment mechanisms to serve a policy-guiding role.

Looking ahead to 2025, policy support will remain critical to sustaining Taiwan’s startup investment momentum. By optimizing capital markets and bridging international channels, it will strengthen startups’ ability to expand overseas and achieve market entry. Amid rapid geopolitical shifts, fast-paced technological change, and intensifying global competition, continuous innovation has become critical for growth. Startups must strengthen their resilience, stay attuned to market dynamics, and iterate quickly to navigate this uncertain future.

1. Deal Count Declines as Investment Volume Reaches a New High

AI has been the standout sector in the global venture capital market in recent years, yet overall market activity remains subdued. Taiwan, however, has followed a different trajectory. A review of Taiwan’s 4,500 startup investment deals from 2015 through the first quarter of 2025, totaling US$18.95 billion[1]. From 263 deals totaling US$880 million in 2015, Taiwan’s startup investment market has surged over the past decade, growing to more than 600 deals in 2024 with a total value of US$3.34 billion, surpassing the NT$100 billion threshold. Deal activity rose sharply in 2019, driven by the NDF’s Business Angel Investment Program. Although the market cooled in 2020 due to the pandemic, investment activity rebounded from 2021 to 2023. Amid elevated global uncertainty and a more conservative venture capital environment, Taiwan recorded 605 startup investment deals in 2024, a decline of about 4.7% from the previous year.

While the decline in deal count reflects a cooling of market sentiment, total investment volume continues to expand. Taiwan’s startup investment volume reached US$3.34 billion in 2024, up approximately 4.5% year-on-year and marking the highest annual amount since 2015. Notable deals during the year include investments in AltruBio, APh ePower, KKday, Botrista, and TXOne Networks. In the first quarter of 2025, investment volume reached US$640 million across 101 deals, with companies such as Taiwan Bio-Manufacturing Corporation (TBMC), Graid Technology, Health2Sync, and Graphen Drugomics each raising more than US$10 million. As Taiwan’s startup ecosystem continues to mature, a growing number of technology-leading or market-leading startups are expected to emerge as key players and attract greater investor attention. Capital is likely to become increasingly concentrated in these high-potential companies.

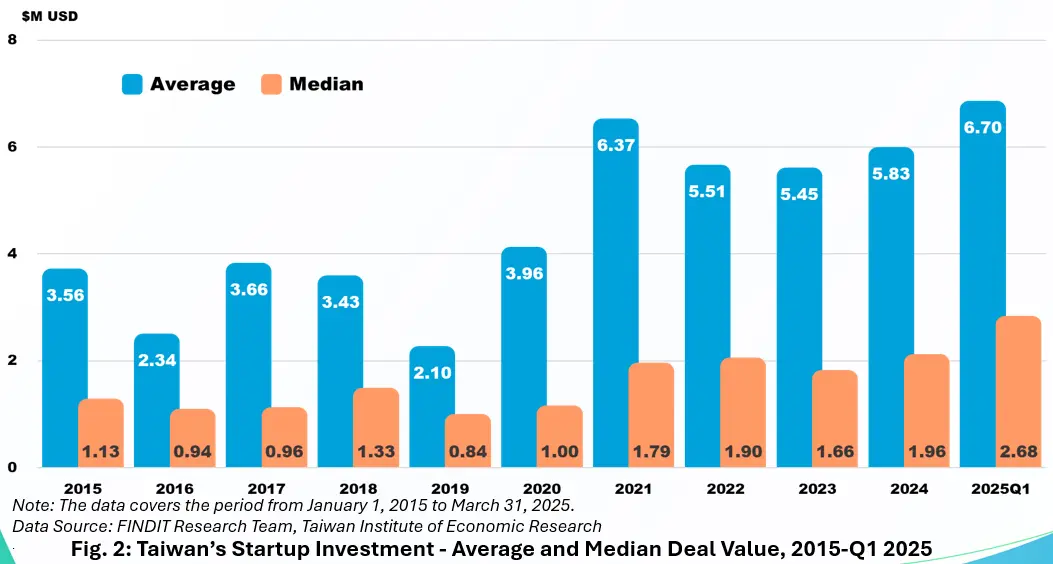

2. Average Deal Size Rises and Mid-Sized Investments Gain Share

In 2024, the average deal size reached US$5.83 million, with a median of US$1.96 million. Compared with 2023, these figures rose by 7% and 18% respectively. In the first quarter of 2025, the average further increased to around US$6.7 million, with a median of US$2.68 million. On the surface, the rise in deal size may appear to signal stronger investor confidence and a willingness to commit more capital. However, given the overall decline in deal count, it also suggests a growing concentration of capital in selected startups. The gap between the average and the median widened from roughly US$3.61 million in 2022 to US$3.87 million in 2024.

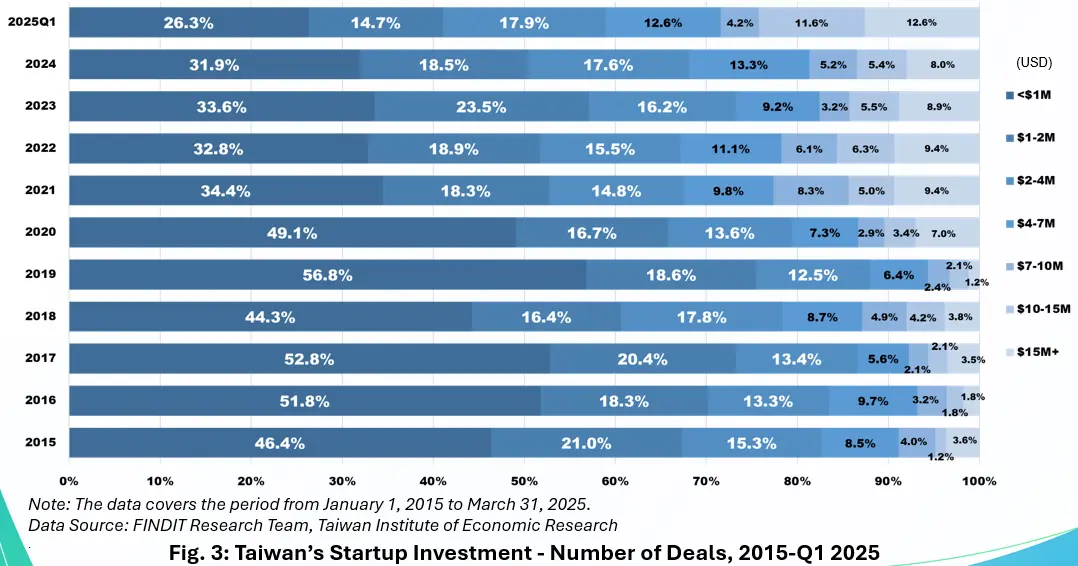

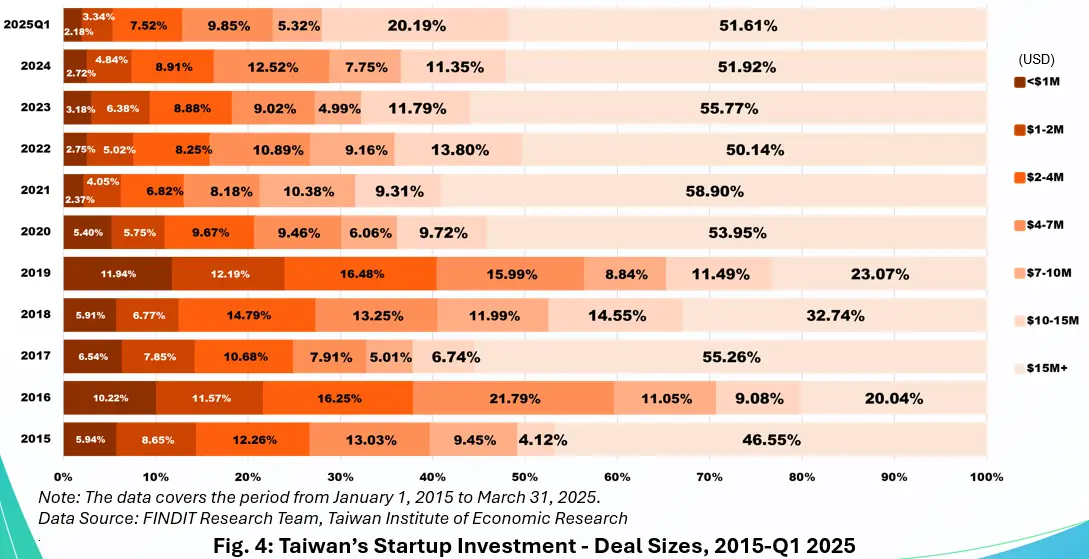

To better understand the distribution of startup investment, deal sizes were categorized, and their shares of total deal count and total investment volume were calculated. In 2024, deals below US$2 million accounted for 50.4% of total deal count, down from 57.1% in 2023. Deals below US$1 million (31.9%) and those between US$1 million and US$2 million (18.5%) also declined from their 2023 levels of 33.6% and 23.5% respectively. In terms of investment volume, deals below US$2 million accounted for 7.5% in 2024, down from 9.6% in 2023. Deals above US$10 million made up 13.4% of total deal count in 2024, slightly lower than 14.4% in 2023, while their share of total investment volume fell from 67.6% to 63.2%.

With overall investment volume rising and both small deals (below US$2 million) and large deals (above US$10 million) declining, capital consequently concentrates in mid-sized deals. In 2024, deals between US$4 million and US$10 million accounted for 18.5% of total deal count, up from 12.4% in 2023. Deals between US$4 million and US$7 million (13.3%) and those between US$7 million and US$10 million (5.2%) both exceeded their 2023 shares of 9.2% and 3.2% respectively. In terms of volume, deals between US$4 million and US$10 million made up 20.3% of total investment in 2024, rising from 14.0% in 2023.

Despite this shift, small deals remain a cornerstone of Taiwan’s startup investment landscape, accounting for roughly half of all deals. However, their share has declined in recent years, while mid-sized deals between US$4 million and US$10 million have gained traction. These startups have typically secured a foothold in their markets and are seeking additional funding to support further expansion.

3. Continued Growth in Energy and Health Biotech; Strong Attention to Communications and Semiconductor Hardware

Among all startup investment sectors, hardware, health care, and energy remain the most prominent areas of focus. From 2015 to the first quarter of 2025, the hardware and manufacturing sector saw a cumulative total of 1,028 deals, the highest among all sectors, with total investment reaching US$3.74 billion. Although both deal count (120) and investment volume (US$613 million) in 2024 declined by roughly 13.0% and 5.2% compared with 2023, the sector remains a key hotspot in Taiwan’s startup landscape. Supported by Taiwan’s mature electronics and industrial manufacturing base, hardware and manufacturing startups continue to attract strong investor interest and align closely with domestic investor preferences. Representative examples include Hon.Precision, which produces semiconductor automation equipment; Eternal Precision Mechanics, known for vacuum lamination technology and laminator manufacturing; and Global Magic, a supplier of passive inductive components.

The global surge in AI interest has also created new market-entry opportunities for Taiwanese startups in related industries. Notable examples include META Green Cooling Technology, which specializes in water-cooling solutions for data centers; AionChip Technologies, a developer of high-speed data-transmission technologies; and AuthenX, which focuses on silicon-photonics solutions.

In addition, communications and unmanned aerial vehicles (UAVs), both within the hardware sector, have gained increasing attention in recent years due to external factors and policy support. Key startups include Tron Future, which develops anti-drone defense systems; AiSeed, focused on UAV inspection and defense technologies; ALifecom, which provides wireless communication signal testing solutions; and Mantaray, a developer of satellite communication technologies.

Health care and biotechnology have long been among the most active sectors in both domestic and global startup investment markets. Given the sector’s substantial capital requirements and high entry barriers, strong demand for cutting-edge technologies and innovative products continues to drive growth. The integration of AI has further sustained investor interest. From 2015 to the first quarter of 2025, Taiwan recorded 898 deals in the health care and biotechnology sector, second only to hardware and manufacturing, with total investment reaching US$4.04 billion. In 2024, the sector saw 127 deals, slightly above the 125 recorded in 2023, and investment volume reached US$743 million, an increase of about 2.3% from the previous year.

Major investments in 2024 and the first quarter of 2025 include AltruBio, which develops innovative immunotherapy drugs; Syncell, known for optical targeting technology and related instrumentation R&D; Yoda Pharmaceuticals, which focuses on new drug development for central nervous system disorders; BIONET Therapeutics, specializing in regenerative medicine and cell-therapy products; and Smart Ageing Tech (Jubo), a company developing software solutions for long-term care providers.

The energy sector has experienced accelerating momentum since 2020, driven by net-zero commitments and rising demand for renewable energy. Beyond wind and solar power, segments such as energy efficiency, energy storage, and energy management have also emerged as major engines of growth. From 2015 to the first quarter of 2025, the sector recorded 501 deals, with total investment reaching US$5.11 billion. In 2024, it saw 106 deals, an increase of 10.4% from 2023, while investment volume reached US$1.076 billion. Although this represented a decline of about 5.7% year-on-year, total investment still exceeded the US$1 billion mark.

Notable deals in 2024 and the first quarter of 2025 include APh ePower, an energy-service provider specializing in aluminum-battery energy-storage technology and carbon-credit services; Stellar Power System, a subsidiary of Chung Hsin Electric & Machinery that develops hydrogen fuel-cell solutions; Smart Harvest, a joint venture between Acer and Green Harvest responsible for planning and operating the Shalun Smart Energy Management System; Blade Hydrogen Green Technology, a hydrogen-energy and fuel-cell startup spun off from the Industrial Technology Research Institute (ITRI); and Patriot Green Energy, which develops high-performance solid-state lithium-ion battery technologies.

Notably, the sustainability and social impact sector, which has grown significantly since 2022 and has become an emerging focus of startup investment in Taiwan. Although the sector recorded only 133 deals totaling US$506 million from 2015 to the first quarter of 2025, it has expanded rapidly. Between 2021 and 2024, deal count increased from 10 to 29, while investment volume rose from US$38.92 million to US$111 million.

Key focus areas of activity include carbon reduction and waste treatment. Representative startups include Sacurn Carbon, which uses carbon-sequestration technologies to convert natural residual materials into carbon-negative products; Thermolysis, which focuses on microwave-assisted pyrolysis technologies to develop high-efficiency carbon-fiber recycling solutions; and Fun Lead Change (ECOCO), which is dedicated to the circular economy and provides a smart-recycling platform for collecting recyclable bottles, cans, cups, and dry batteries.

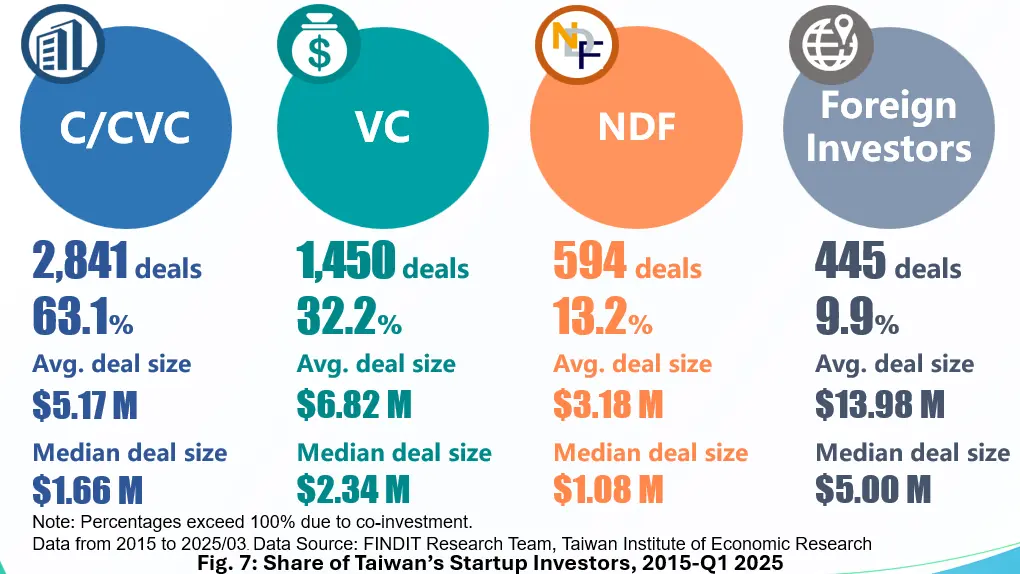

4. Venture Capital and Foreign Investment Weaken, While Corporate Venture Capital Remains a Key Pillar

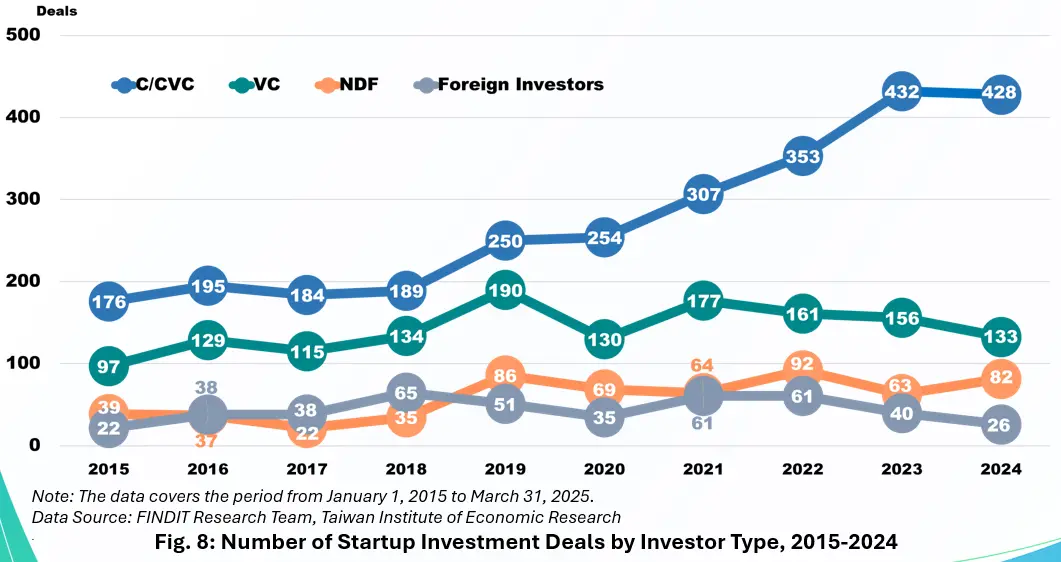

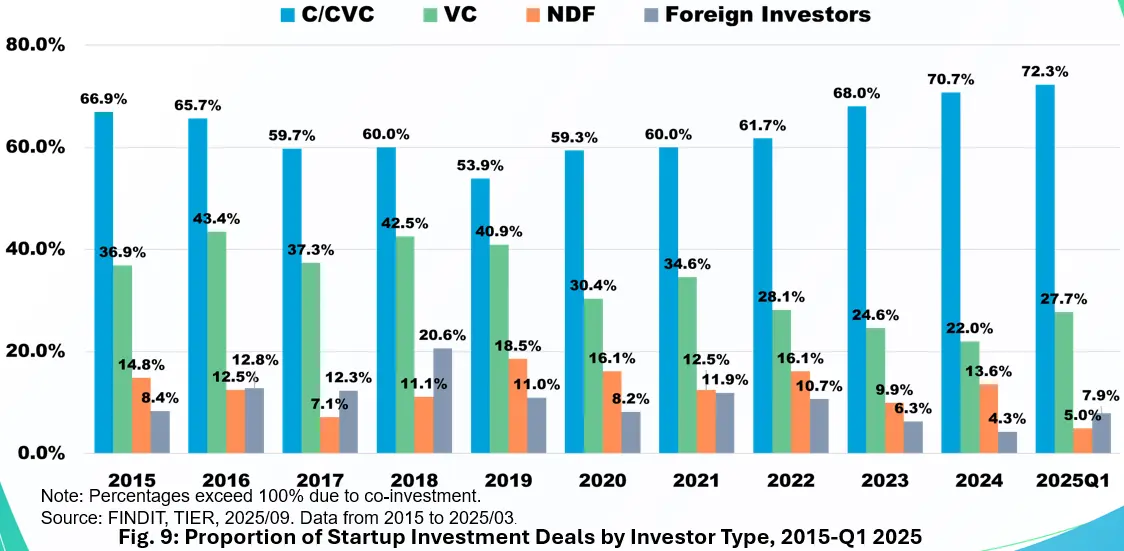

Among the 4,500 startup investment deals analyzed between 2015 and the first quarter of 2025, corporate and corporate venture capital (C/CVC) investors participated in 2,841 deals, accounting for approximately 63.1% of total deal count. The average deal size reached US$5.17 million, with a median of US$1.66 million. C/CVC activity is concentrated in hardware and manufacturing, with a cumulative 750 deals, reflecting Taiwan’s long-established industrial base. This is followed by health care and biotechnology (515 deals) and the energy sector (429 deals), supported in part by growing demand for green-energy transition. In terms of trends, C/CVC participation has steadily increased over the years, rising from 184 deals in 2017 to 432 deals in 2023, before edging down slightly to 428 deals in 2024. Their share of total deal count grew from 53.9% in 2019 to more than 70% (70.7%) in 2024, and further to 72.3% in the first quarter of 2025.

Venture capital (VC) firms, both domestic and international, participated in 1,450 deals from 2015 to the first quarter of 2025, accounting for 32.2% of all transactions. The average deal size reached US$6.82 million, with a median of US$2.34 million. VC investments were concentrated primarily in health care and biotechnology (345 deals), followed by hardware and manufacturing (243 deals). Many of these involved co-investments with C/CVC investors, including deals in companies such as Protect Biotech, MedicalTek, Graid Technology, and Chip-GaN Power Semiconductor.

Over the past decade, VC activity reached its peak in 2019 with 190 deals, driven in part by the NDF’s Business Angel Investment Program. Although the pandemic dampened investment in 2020, deal count rebounded to 177 in 2021. In subsequent years, however, VC participation began to decline. By 2024, VC investors were involved in 133 deals, a decrease of 14.7% from 2023, and their share of total deal count fell from 34.6% in 2021 to 22% in 2024.

A similar downward trend is evident among foreign investors. From 2015 to the first quarter of 2025, foreign investors participated in 445 deals, representing about 9.9% of total investments. Foreign investors tend to target startups with more mature products, established operations, or strong international expansion potential, resulting in larger deal sizes. Their average investment reached US$13.98 million, with a median of US$5 million. Participation has fallen notably over the past two years: foreign investors took part in only 26 deals in 2024, a 35% decline from the 40 recorded in 2023, and their share of deal count dropped from 11.9% in 2021 to 4.3% in 2024.

The National Development Fund (NDF) plays a pivotal role in shaping Taiwan’s startup investment market and ecosystem. Through initiatives such as the Business Angel Investment Program, the NDF not only invests directly in startups but also mobilizes capital from C/CVC and VC investors, helping catalyze early-stage entrepreneurship. Through its fund-of-funds (FOF) structure, the NDF channels capital to startups via professional investment institutions, supporting their growth. The NDF has also advanced multiple thematic initiatives, providing support across SMEs, strategic manufacturing, strategic services, and cultural and creative industries, as well as newer areas such as AI startups, smart robotics, and green growth.

From 2015 to the first quarter of 2025, the NDF participated in 594 startup investment deals, representing 13.2% of the total. The average deal size was US$3.18 million, with a median of US$1.08 million. Its investments have been concentrated primarily in health care and biotechnology (147 deals) and hardware and manufacturing (100 deals). In recent years, NDF participation has shown clear growth. In 2024, the NDF was involved in 82 deals, a 30.2% increase compared with 2023. Its share of total deal counts also rose, growing from 9.9% in 2023 to 13.6% in 2024.

5. Conclusion

Taiwan’s startup investment exceeded NT$100 billion (US$3.34 billion) in 2024, an increase of 4.5% from 2023 and the highest level in the past decade. Although the number of deals declined, Taiwan’s startup investment market has remained relatively resilient amid the global downturn in venture capital, and the ecosystem has continued to strengthen through the efforts of stakeholders across sectors. Nevertheless, as a “startup island,” Taiwan still faces several challenges that require further attention.

The first challenge is boosting venture capital participation. VC investment, which typically targets high-growth opportunities, is a critical driver of startup development. As the share of VC involvement in overall deal count continues to decline, Taiwan must adopt new policy measures to mobilize greater participation from startup investors through capital-based mechanisms, while building a stronger pipeline of investable startups to drive positive ecosystem cycles and iteration. Beyond recent amendments to the Statute for Industrial Innovation aimed at improving Taiwan’s startup investment environment, the NDF has introduced several multi-10 billion-NT-dollar investment initiatives expected to play a catalytic role in stimulating future activity. In addition, the National Development Council’s “Startup Bloom Program” is set to further enhance the environment for nurturing emerging startups.

The second challenge internationalization. Taiwan currently offers a wide range to support startups in their global expansions, including programs for business development, training, exhibitions, competitions, overseas hubs, and investment partnerships. In parallel, several VC firms have extended their international presence, helping raise Taiwan’s visibility as a startup island. However, this growing presence has yet translated into greater engagement from foreign investors. To address this gap, Taiwan must deepen its understanding of different markets and business conditions, while improving mechanisms that connect domestic startups with opportunities for overseas expansion and identifying teams with proven execution capabilities for global growth. As Taiwan seeks to play a stronger role as the gateway for startups entering overseas market, it should strengthen the linkage between policy support and actual market entry by reinforcing bridging channels and engaging key talent.

As global geopolitical conditions and technological landscapes continue to evolve rapidly, the urgency of innovation intensifies. Looking ahead to 2025, the startup investment environment will remain uncertain, and global competition is likely to grow even fiercer. Policy support will continue to serve as a cornerstone of Taiwan’s startup ecosystem, creating opportunities to maintain market activity and uncover growth-oriented innovations through new investment initiatives. Ultimately, startups must build greater resilience, stay alert to market shifts, and accelerate the iteration of products, technologies, and business models, whether or not they expand overseas. Only by adapting quickly to evolving market conditions can startups navigate uncertainties and meet future challenges.

Note [1]:

The transactions reviewed include:

-

Companies registered in Taiwan, or registered overseas but founded by individuals from Taiwan;

-

Private equity investment made prior to a company’s public listing (including OTC and emerging stock market listings), excluding debt financing, convertible bonds, subsidies, and ICOs.

-

Acquisitions and 100% investments from a parent company into its subsidiary are excluded.

Data sources include: (1) International startup databases; (2) News media; (3) Invested companies and investment institutions; (4) Investment disclosures of listed and OTC companies; (5) National Development Fund quarterly/annual reports; (6) Company registration information from the Administration of Commerce, Ministry of Economic Affairs; (7) Startup deal-flow platforms.