【2025 Taiwan Startup Investment Trends Annual Report – Defense & Military】UAVs in the Sky, Smart Surveillance on the Ground Strengthen National Security

Amid rising global geopolitical tensions and lessons from the war in Ukraine, the defense and military industry has become a critical component of national security and technological innovation. Leveraging its strengths in semiconductors and precision manufacturing, and supported by President Lai Ching-te’s “Five Trusted Industry Sectors” policy, which designates defense as a core strategic sector, Taiwan’s defense budget reached a record high of NT$949.5 billion in 2025. Defense spending as a share of GDP is expected to increase to 5% by 2030.

![[ 2025 Taiwan Startup Investment Trends Annual Report – Defense & Military ]UAVs in the Sky, Smart Surveillance on the Ground Strengthen National Security](https://findit.org.tw/Files//UploadFile/Findit-fa29ddbd-1024-4e04-8773-2af690923942.webp)

Amid rising global geopolitical tensions and lessons from the war in Ukraine, the defense and military industry has become a critical component of national security and technological innovation. Leveraging its strengths in semiconductors and precision manufacturing, and supported by President Lai Ching-te’s “Five Trusted Industry Sectors” policy, which designates defense as a core strategic sector, Taiwan’s defense budget reached a record high of NT$949.5 billion in 2025. Defense spending as a share of GDP is expected to increase to 5% by 2030.

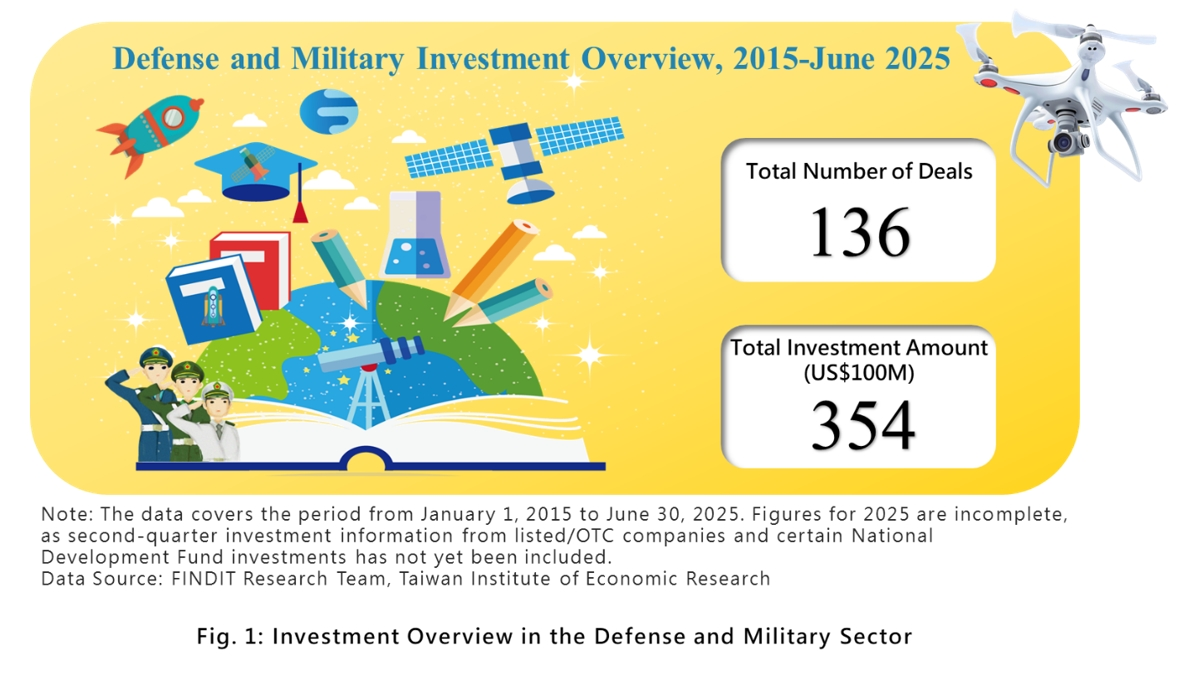

Driven by both policy support and market demand, investment activity in Taiwan’s defense and military startups has gained momentum. Between 2015 and the first half of 2025, a total of 136 deals were recorded, with cumulative funding reaching approximately US$354 million. Beyond its role as a cornerstone of national security, the defense sector is also generating broader economic benefits through the integration of UAVs, Low Earth Orbit (LEO) satellites, and AI technologies, positioning Taiwan as an increasingly important player in the global democratic technology alliance.

1. Geopolitical Tensions Drive Investment, Early-Stage and Small-Scale Deals Dominate

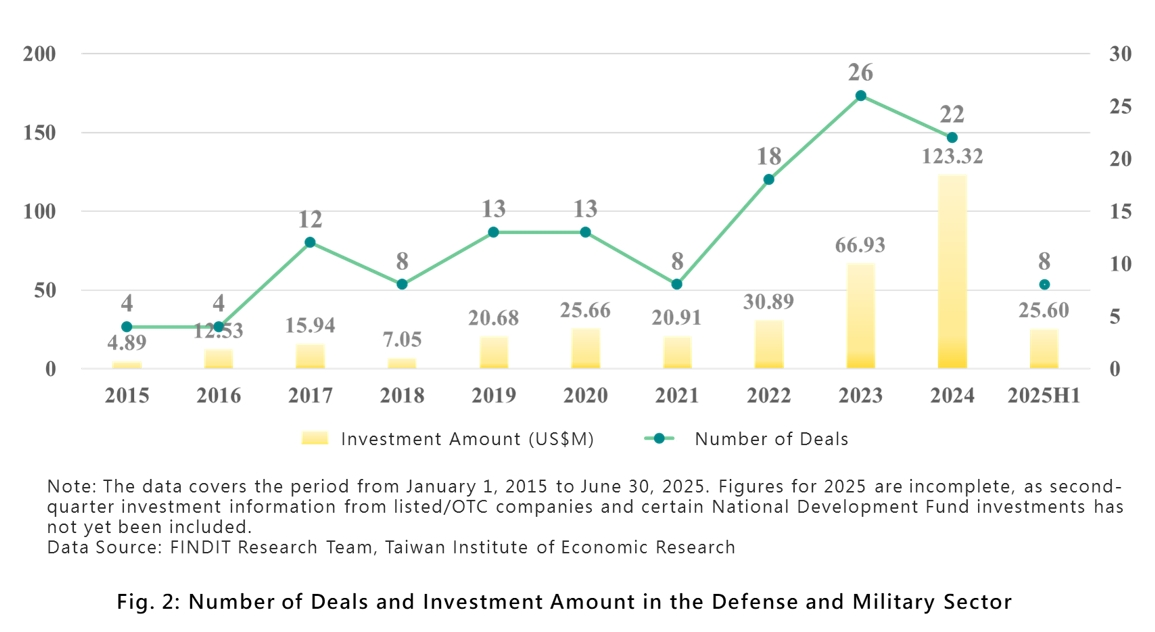

A review of investment trends shows that the outbreak of the war in Ukraine in 2022 marked a key turning point. The number of deals rose to 18 in 2022 and further increased to a peak of 26 in 2023, indicating accelerated capital inflows into startups of strategic importance. Investment activity is highly concentrated in early-stage rounds (pre-Series A and earlier), accounting for 81.62% of total deals and approximately 70% of total funding. This suggests that the industry remains in the early stages of technological development and innovation.

Deal sizes in this sector remain relatively small, with 65.44% of transactions below US$2 million, indicating a market dominated by small-scale, exploratory investments. At the same time, seven deals exceeding US$10 million suggest that select companies with breakthrough technologies are beginning to attract larger-scale capital. Corporate investors, including domestic corporations and corporate venture capital (CVC), have been particularly active, participating in approximately 63.97% of deals. Major electronics companies such as Foxconn and Wistron are investing to enter the UAV supply chain, reflecting broader efforts to drive industrial upgrading and cross-sector integration.

2. Unmanned Vehicles Lead in Deal Count, While Defense Aerospace Attracts Larger Investments

Across subsectors, unmanned vehicles lead with 53 deals, making them the most active segment, driven by the widespread use of drones in military reconnaissance and commercial logistics. The subsector includes a growing number of startups, such as GEOSAT Aerospace & Technology and AiSeed, and extends into unmanned vessels and control systems, forming a comprehensive ecosystem.

Defense aerospace ranks second in deal count but stands out for its capital intensity. With an average deal size of approximately US$3.94 million and total funding reaching US$197 million, the subsector continues to attract substantial investment, driven by high technical barriers and the strategic importance of technologies such as LEO satellite communications and millimeter-wave solutions. The defense applications subsector recorded 33 deals, focusing on key technologies such as cybersecurity and precision manufacturing. Representative companies include CyCraft Technology and DPS, highlighting the growing integration of software and hardware in defense technologies.

3. Industry Leaders Forge Strategic Partnerships, Dual-Use Technologies Become Central

Among the top ten deals over the past two years (2024 to H1 2025), investments are highly concentrated in UAVs and advanced communication technologies, with many led by listed companies as strategic investors. For example, GEOSAT Aerospace & Technology secured NT$1 billion in funding from Wistron to accelerate mass production and international expansion of unmanned vehicles. Tron Future Tech, leveraging its AESA radar and anti-drone systems, completed a NT$900 million Series A round and secured nearly NT$1 billion in contracts from the Ministry of National Defense, successfully translating its technology into defense orders.

In the millimeter-wave communications segment, companies such as TMY Technology and Pyras Technology have received investments from major corporations, including Inventec and Gemtek Technology, highlighting Taiwan’s critical role in the LEO satellite supply chain. In addition, AI-powered drone company AiSeed and military-grade drone developer Giga-Image have received backing from Pegatron and GIGABYTE, respectively. These developments underscore how collaboration between ICT corporations and defense technology startups has become a key driver of industrial adoption.

4. Policy and Capital as Dual Engines Strengthen Taiwan’s Position in Non-PRC Supply Chains

Taiwan’s defense and military industry is at a pivotal stage, marked by leadership in unmanned technologies, growing aerospace capabilities, and expanding application scenarios. Through initiatives such as the “Five Trusted Industry Sectors” policy, the Asia UAV AI Innovation Application R&D Center, and various national defense programs, the government is providing strong policy support and real-world testing environments.

As global supply chains continue to restructure and demand for non-PRC (“non-red”) supply chains grows, Taiwan’s startups, by leveraging their strong foundations in semiconductors and ICT and with continued support from capital markets, can accelerate commercialization and deepen the integration of dual-use technologies. This, in turn, positions Taiwan to establish a strategically indispensable role in the global defense and aerospace value chain, creating a virtuous cycle in which national defense supports economic growth and economic strength reinforces national defense.