【The Startup Column: Taiwan’s Startup Hubs and Accelerators – 2024 in Review】

Since 2019, FINDIT has consistently provided valuable insights for those interested in the development of Taiwan's startup ecosystem. Through data disclosure, the platform delivers timely updates that spotlight key elements of the entrepreneurial landscape.

This article offers a continuation and update to earlier pieces in the series, including “How Many Accelerators in Taiwan?”, “58+3! Not the Heat of Romance, Not the Strength of Kaoliang; It's About Accelerators...”, and “Startup Ecosystem Review: A Deep Dive into Taiwan's Startup Hubs”

Based on the concept of “hubs” (also known as startup bases or communities) to map Taiwan’s startup landscape, and excluding regional revitalization hubs due to their distinct purposes, there are 49 hubs (52%) in the northern region, 15 hubs (16%) in the central region, 25 hubs (26%) in the southern region, and 3 hubs (3%) each in the eastern region and outlying islands as of May 2024.

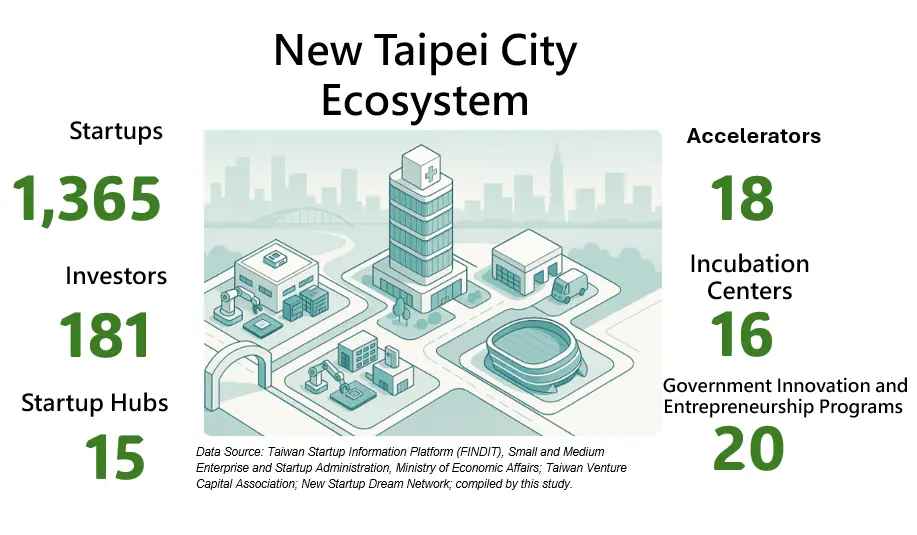

A closer look at the distribution by city and county shows that Taipei City leads with 24 hubs, followed by New Taipei City with 11, Taoyuan City with 9, Kaohsiung City with 8, and Tainan City and Taichung City with 7 each. Miaoli County and Pingtung County each host 6 hubs, while Chiayi County and Yilan County each host 3. Penghu County, Hsinchu City, and Yunlin County each host 2, and Taitung County, Changhua County, Hsinchu County, Kinmen County, and Hualien County each host 1. In total, Taiwan is home to 95 startup hubs.

Regarding the types of operators, 31 hubs (33%) are operated by the central government, 60 hubs (63%) are primarily managed by local governments, 3 hubs (3%) are run by universities, and 1 hub (1%) is operated by the private sector. As of the end of May 2024, the majority of active startup hubs were established during the peak period between 2016 and 2018, with 19 founded by the central government, 18 by local governments, and 3 by universities. In comparison, during another period of growth from 2021 to 2023, 2 hubs were established by the central government and 31 by local governments.

Further analysis reveals that 12 out of the 95 startup hubs (13%) possess international support capabilities. This evaluation is based on whether these hubs have organized activities such as international forums (online/offline), matchmaking events, mentorship and networking opportunities, or collaborated with the government to assist with entrepreneur visa applications.

The startup hubs with international mentoring capabilities include: Startup Terrace Kaohsiung, Startup Terrace Linkou, N/S Terminal, FinTechSpace, Taiwan Tech Arena (TTA), Taiwan Startup Stadium (TSS), Center for Innovation Taipei (CIT), NPO HUB Taipei, TXI Center, National Biotechnology Research Park, TTA South, and the AAMA Taipei Cradle Program (Taipei Co-Creation Foundation for Entrepreneurs, TCCFE).

Analyzing the key sectors, 24 startup hubs (25%) are categorized as cross-industry, supporting startups without limiting to any particular fields. These hubs include: Hsinchu Science Park Youth Entrepreneurship Base (Yilan Entrepreneur's Studio), Hualien Innovation Base (Hualien County Government Youth Development Center), Kinmen Youth Hub, Miaoli County Youth Entrepreneurship Command, Taoyuan Youth Entrepreneurship Command Center/Youth Entrepreneurship Resource Center, Startup Terrace Linkou, InnoSquare, Hsinchu Science Park Youth Entrepreneurship Base (Young Entrepreneur's Studio), Hsinchu Startup Hub, CCU Startup Land, Taiwan Tech Arena (TTA), Taiwan Startup Hub, Taiwan Startup Stadium (TSS), Taipei Co-Space, t.Hub Taipei, Center for Innovation Taipei (CIT), Tatung University Youth Innovation Base, TTMaker, Southern Taiwan Innovation & Research Park (STIR), Win Win Innovation & Incubation Base, Southern Taiwan Science Park (STSP) Startup Workshop, TTA South, AAMA Taipei Cradle Program, and STARTUP@NCHU. Beyond the cross-industry field, the majority of startup hubs operate as theme-based clusters, with 71 such hubs, accounting for 75% of the total.

Among these theme-based hubs, the Cultural and Creative sector leads with 26 hubs (28%), followed by Robotics/AIoT/Smart Automotive with 10 hubs (11%), and Social Innovation with 8 hubs (9%). Both 5G/AIoT/Digital Content and Maker each account for 6 hubs (6%), while Market Expansion/E-commerce has 5 hubs (5%). FinTech/Blockchain, Biotech/Medical, and Digital Transformation each comprise 2 hubs (2%). The “Other” category includes 4 hubs (4%).

An Overview of Startup Accelerator Development

A review of the operational status of startup accelerators and acceleration programs (hereafter collectively referred to as “accelerators”) identifies a total of 83 accelerators still active as of the end of May 2024. This information was compiled from publicly available sources, including Facebook pages, official websites, event platforms, and the Government e-Procurement System.

Trends in accelerator establishment over the years point to steady growth, with 2018 standing out as the peak. That year alone saw the launch of 13 accelerators, including BE Accelerator, SparkLabs Taiwan, HAOSHi Accelerator, Chunghwa Telecom 5G Accelerator, HYPE Global Virtual Accelerator, Mosaic Venture Lab, SYSTEX AI+ Generator Program, Rapid Program, Taiwan Accelerator Plus (TAcc+), CnC Club, G Camp, GlintMed Accelerator, and the S2B Startups To Business Accelerator, founded by the Footwear & Recreation Technology Research Institute. Beyond 2018, both 2023 and 2024 experienced double-digit growth, with 10 and 11 new accelerators established.

Regarding government support for accelerators, central government agencies such as the National Science and Technology Council, the Ministry of Education, the Small and Medium Enterprise and Startup Administration, and the Ministry of Culture, as well as local governments like New Taipei City, Taoyuan City, and Hsinchu County, have fostered startup growth and acceleration by either establishing or subsidizing accelerators. Among the active accelerators, 44 are either government-established or receive government subsidies, accounting for 53%, while 39 accelerators (47%) operate without government support.

An analysis of accelerator locations reflects the primary regions where startups are concentrated. In the northern region, which includes Taipei, New Taipei, and Taoyuan, there are a total of 67 accelerators. Kaohsiung, one of the six metropolitan areas, hosts 4, while Tainan and Taichung each have 2. Overseas, there are the CDIB Japan Innovation Accelerator, a collaboration between the CDIB Capital Innovation Accelerator and the CCIA Tokyo Innovation Hub, as well as Rocketindo, which focuses on the Indonesian market. In terms of support capabilities, 46 accelerators (55%) offer international support, while 37 accelerators (45%) do not focus on assistance related to international development.

Previous reviews show that the total number of accelerators has remained stable (as of June 2023, there were 78 active accelerators in Taiwan, compared to 85 in December 2022.), suggesting that the demand for accelerator operations and services remains strong. However, with the rapid evolution of new technologies and emerging sectors, the structure of accelerators may also be undergoing changes. To better understand the current state of accelerator development, the following section offers further analysis based on the type of operator and the industries or areas of focus.

Unlike incubation centers, where startups may participate for several years, accelerators typically run short, intensive programs lasting three to six months. These are designed to push startups toward rapid growth under high-pressure conditions, similar to cram schools preparing students for critical exams. However, with increasing globalization, specialization, high risk, and low profitability, accelerators once seen as extensions of venture capital firms have undergone significant transformation. There has been a notable rise in specialized accelerators and those backed by large corporations, while traditional investment-driven accelerators, which operate on a regular basis, have become less common. To further understand the development of accelerators in Taiwan, this report categorizes them into four types based on their resources and strengths: Investment-Oriented, Academic/Research-Driven, Corporate-Linked, and Resource and Mentorship-Based. Each category will be discussed in detail in the following sections.

Among the four types, Resource and Mentorship-Based accelerators are the most common, totaling 37 and accounting for 45%. They are followed by Corporate-Linked accelerators with 19 (23%) and Academic/Research-Driven accelerators with 16 (19%). The least common are Investment-Oriented accelerators, with 11 (13%). According to data from previous studies conducted in 2019 and 2020 (Hsu, 2019; Hsu & Liu, 2020), the total number of accelerators increased from 48 in 2019 to 61 in 2020, and further to 84 in the 2024 review. Among the four categories, only Corporate-Linked accelerators showed no growth in number.

Notable companies that have played an active role in accelerator development include HTC, YongLing Foundation, and Foxconn Technology, each of which participated in the establishment of accelerators in 2016. They were followed by ChungHwa Telecom and SYSTEX Corporation in 2018, and MIGHT ELECTRONIC in 2019. These firms are among the most established players in supporting startup growth through accelerator programs.

The focus areas of accelerators vary based on the objectives of their founders and participants. Analyzing the sectors these accelerators engage with, more than half (45 accelerators, accounting for 54%) do not restrict their support to specific fields, often working with startups across four or more sectors. As long as a startup demonstrates innovation in its business model or technology, it is generally considered eligible for support.

Ranked second is Biotech/Medical, with 9 accelerators (11%), reflecting both domestic and global trends in early-stage investment. If early-stage investors and startup nurturers are willing to engage in the biomedical industry, startups in this sector may have greater potential for growth. This suggests that the biomedical industry will be one of the key contributors to Taiwan’s future growth momentum.

The third most prominent sector is Ageing/Healthcare, supported by 7 accelerators (9%). The growth in this sector is closely tied to government policy. Food/Agriculture and Internet/ICT follow, with 4 accelerators each (5%).

Further analysis of operator types reveals that single-type operators may face limitations in terms of resources, industry focus, and expertise. To address these constraints and enhance innovation and commercialization, cross-industry and interdisciplinary collaboration is considered an effective strategy. For example, nonprofit organizations, foundations, management consultants, and professional service providers offering accounting, legal, or patent-related consulting often partner with venture capital firms, accelerators, or corporations to jointly operate accelerators and pursue shared goals.

Key Observations and Conclusions

Within the startup ecosystem, startup hubs, incubation centers, and accelerators play distinct roles. In terms of support duration, startup hubs offer the longest assistance, followed by incubation centers, while accelerators offer the shortest support cycles, typically three to six months and rarely over one year.

Given the widespread distribution of startup hubs across Taiwan, understanding and engaging with the local entrepreneurial ecosystem is a fundamental responsibility for startups. As many of these hubs are established with support from central or local governments, they also play a crucial role in channeling and localizing policy-driven resources. As a result, empowerment has emerged as a core capability that startup hubs must continuously strengthen. This approach enables regionally focused hubs to collaborate with internationally oriented hubs and overseas outposts, forming a more cohesive and integrated network of resources and services. For example, a startup hub may refer locally incubated startups to hubs with international capabilities or to overseas offices. Likewise, overseas offices may introduce international startups interested in entering the Taiwanese market to these internationally connected hubs. Furthermore, when production or development requires local industry linkages, regionally focused hubs can serve as valuable connectors.

As for accelerators, collaboration with startups represents a compelling strategy for established companies seeking transformation or long-term growth. By leveraging government-funded programs, enterprises can collaborate with startups through accelerator operations, while also incorporating academic and research expertise to develop new products or production models. On one hand, startups can accelerate proof-of-concept processes and identify early market needs. On the other hand, enterprises gain opportunities to experiment across different domains, gradually shaping future development directions and sources of growth.