登入

登入

Ping-Hang Fan (Deputy Director of Division VI, Taiwan Institute of Economic Research)

Industries and the capital market are going through rapid changes with the initiation of new economic models. Various startup businesses are brought forth in this environment, and not only have they carved out certain market share among intense competition, they have also stood out among competitors to become disrupters to traditional industries and have created unique, innovative value. This trend of entrepreneurship started out in Silicon Valley, Israel, and China, and created a group of 'unicorn companies,' hailed by entrepreneurs and investors. This list includes famous car-hailing service Uber and DiDi Chuxing, short-term house rental service platform Airbnb, cashflow technology Stripe, and business collaboration platform Slack.

In recent years, the Taiwanese government strove to promote an entrepreneurial ecosystem. From the perspective of policy advocacy, 'funds' are critical elements that need to be controlled. In addition, funds are also the greatest stimuli for entrepreneurs and investors alike. To the investors, it is crucial to monitor and evaluate the activities in a capital market and changes in industry trends, helping them to review possible target objectives to ensure that positive rewards can be reaped from investments. To the entrepreneurs, achieving external investments is often a necessary path toward growth, while maintaining an understanding of active investors, innovative trends, and achieving funds are lessons that startup founders need to learn. Alternatively, the government institution's responsibility lies in the design of the mechanism, allocation of resources, and implementation of policies. And to avoid being out of touch with the market, the drafting of relevant policies needs to be established and adjusted in accordance with capital market movements.

In other words, the transaction information of early-stage capital market is inevitable to the entrepreneurial ecosystem. Such information includes the global early-stage investment database CrunchBase, PitchBook, DealRoom, regular investment trend reports from Preqin and KPMG, and MoneyTree Report from PwC and CB Insights. Nevertheless, comprehensive startup investment information has been long absent from Taiwan. And in the past, statistics from various institutions have often grasped only a part of the information from the early-stage capital market.

To this means, the FINDIT research team from Taiwan Institute of Economic Research (TIER) has continuously studied the funding status of Taiwan’s startups. This data is cross-referenced and compared against global early-stage investment database, information from investment agencies, government investment reports, and company registration information and more, and relevant reports have been released in turn. For this year, the research team has also analyzed the investment information from companies listed on the TWSE and TPEx from the fourth quarter (Q4) of 2014 to the first quarter (Q1) of 2019 for the first time, and incorporated this information into the Taiwan startup funding data to construe an even more comprehensive early-stage capital market overview.

Of the hundreds of thousands of data analyzed, the FINDIT team has found 1,154 early-stage investment deals totaling over US $3.3 Billion, of which 792 are deals in which the startup was founded after 2010 (if you just look at just these 792 companies, they totaled US $2.3 Billion).

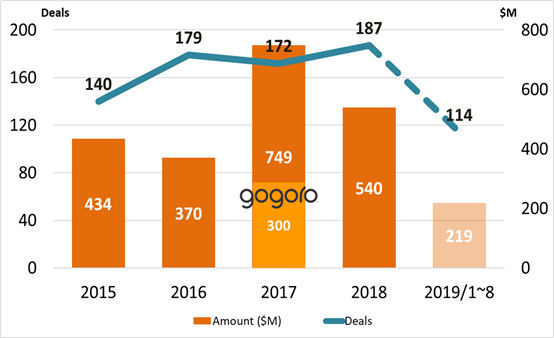

In 2015, there were 140 startup investment deals in Taiwan totaling US $434 million. Since then, Taiwan has seen a steady growth rate in the amount of capital invested in early-stage startups. In fact, by 2018, there were 187 startup investments deals totaling US $540 million! However, in 2016, the amount of investments dipped to US $370 million due to slow market conditions. Also, the large spike in 2017 can be attributed to Gogoro receiving US $300 million. If we exclude this large Gogoro deal from 2017, the total annual growth rate from 2017 to 2018 would be at 20.27%.

Compared to the global market, the amount of startup investments (both the total amount of money invested as well as the number of investment deals) in Taiwan is roughly around the global average. According to the 2018 MoneyTree Report by PwC and CB Insights, the global total number of VC investments was 14,247, a 9.52% increase compared to 2017. These investments amounted to a total of US $207.1 Billion, a 20.69% increase compared to 2017.

Note: Data from 2015 to 2019/8/23, and includes the investment by listed companies to 2019 Q1.

Source: TIER FINDIT

Image 1. Startup Investment in Taiwan by Deals and Amount

Within the investment scale of a single transaction, the amount of money and number of transactions are inversely proportional; most deals are under US $1 million, followed by deals between US $1 to 2 million. Although there are still transactions above US $10 million in Taiwan, most of the investment deals are still rather small compared to the West. According to Preqin's statistics, the average global transaction amount of VC investment in the seed/angel round in 2018 was US $2.3 million, with seed/angel round investment deals accounting for 35% of the total startup investments. The average global transaction amount of a typical Series A amounted to US $16.1 million, and accounted for 28% of the total investment deals. In Taiwan, deals are significantly smaller, though we are seeing investment deals above US $10 million steadily growing year over year.

Note: Data from 2015 to 2019/8/23, and includes the investment by listed companies to 2019 Q1.

Source: TIER FINDIT

Image 2. Startup Investment in Taiwan by Deal Size

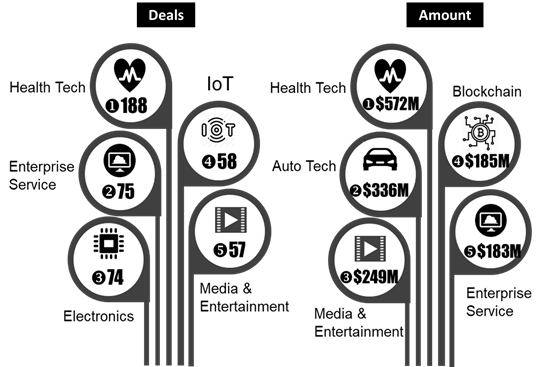

Taiwan’s top industry in terms of VC funding received is the healthcare and medical industry. Whether in total amount of money invested or total number of investment deals, the healthcare and medical industry tops both categories. Since 2015, there are a total of 188 cases totaling US $572 million.

Aside from healthcare, we’ve found that startups that provide software/hardware B2B services or startups that produce electronic components also attracts investors. Startups that focus on blockchain technology also attracts VCs, with a total of US $185 million total invested in the last 4 years.

More importantly, in 2018 alone, Taiwanese blockchain startups collectively attracted over $100 million US dollars; startups like OwlTing and BitoEX are both good examples.

Note: Data from 2015 to 2019/8/23, and includes the investment by listed companies to 2019 Q1.

Source: TIER FINDIT

Image 3. Startup Investment in Taiwan by Industries

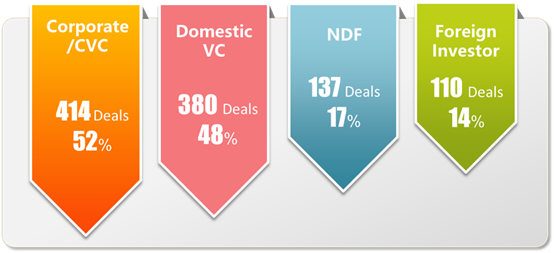

So, who exactly is investing in these Taiwanese startups? The percentage of local companies or Corporate Venture Capital that engages in startup investment is quite high, landing at around 52% of total startup investment deals; VCs come in second at around 48%. The government is also quite active in startup investments. Taiwan’s National Development Fund (NDF) is quite active in the early-stage investment scene, investing in around 17% of total startup investments.

Note: 1. Data from 2015 to 2019/8/23, and includes the investment by listed companies to 2019 Q1.

2. Due to the co-investment, the aggregate number is larger than 100%.

Source: TIER FINDIT

Image 4. Startup Investment in Taiwan by Types of Investors

Ultimately, as the startup ecosystem becomes more robust, we have started to see more and more new startup ventures that have been attracting the attention of investors, both local and foreign. Taiwanese startups have been doing well in attracting investments in the past two years, yet the scale of a single transaction is still rather small compared to the rest of the world. Looking from an investor’s perspective, high risk, high reward, and high technological barriers are still the most attractive to investors looking to invest in Taiwanese startups, such as biotech companies.

To conclude, it is important to combine startups with existing mature industries in Taiwan. As our research has uncovered, corporates and CVCs are the most active investors with B2B startups receiving the most of the funding. These startups receive massive support from big corporates when they were first founded; they’re core value is not to challenge the existing industry, but to solve a specific pain point for the corporation. These kinds of startups may not make the headlines, but are still key to Taiwan’s early investment market.